The Bankruptcy Discharge? Just what Debts get Discharged?

Published • Updated

Why are you filing bankruptcy? As a Detroit bankruptcy attorney, this is one of the first questions I ask a client when they come in for their initial bankruptcy consultation. The typical answer that I get in response is “because I cannot afford to pay my creditors”. But just what is the goal in a typical consumer bankruptcy case? The answer is to obtain a federal court order called a Bankruptcy Discharge. It’s a simple piece of paper, usually two pages, but it has a lot of power behind it (click here for sample discharge). It is an Order signed by a Federal Bankruptcy Judge (a United States Judge) that prevents your creditors from collecting the discharged debts from you now or forever in the future. The discharge order will be granted in nearly 100% of the Chapter 7 consumer bankruptcy cases my office files and is a very powerful document. Because it is a Federal proceeding based in the United States Bankruptcy Court, it also applies to lower courts. Civil judgments obtained by creditors in State of Michigan courts can be discharged in bankruptcy as well.

The Bankruptcy Discharge: Defined.

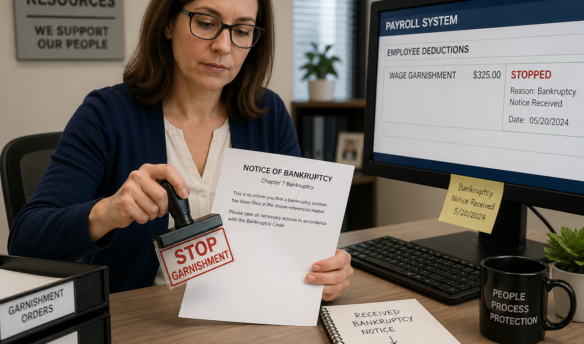

The bankruptcy discharge operates as a release to the debtor from their personal liability for various specified debts. The debtor(s) (the individual filing or if married and filing jointly husband and wife) are not legally required and cannot be forced to repay any debts that are discharged by operation of law. The discharge acts as a permanent order that prohibits all creditors from exercising any form of collection activity on those debts that have been discharged by order of the bankruptcy court, including prohibiting any further legal action or communications with the debtor (including harassing telephone calls, collection letters, etc.)

Although a debtor is no longer personally liable for discharged debts, a properly secured lien (i.e., a charge upon specific property to secure payment of a debt most commonly a mortgage or car loan) will survive after the bankruptcy case and the secured creditor may enforce the lien to recover the property secured by the lien (i.e. foreclose or repossess). So, if you want to keep your house or car, be sure to continue to make the payments after the bankruptcy filing.

What debts will be Discharged in Bankruptcy?

Generally, a bankruptcy discharge will result in the wiping out of the vast majority of your debt including:

- Credit card debt

- Medical bills

- Past due utility bills (you will keep your service)

- Personal loans

- Signature lines of credit

- Payday advance loans

- Repossessed or voluntarily surrendered car debt

- Mortgages that have been foreclosed or you walked away from

- Civil Court Judgments related to any of the above

A few debts will not be discharged by operation of the bankruptcy court order, and will survive the bankruptcy.

These Exceptions to Discharge generally are:

- Child or spousal support and alimony

- Student loans

- Tax debts incurred within the past few years

- Debts related to personal injuries or death caused by drunk driving or other intoxicants

- Court fines and penalties, criminal restitution

- Traffic and parking tickets (Michigan Driver responsibility fees are presently dischargeable)

- Condo or homeowners association dues

There are some other exceptions to a bankruptcy discharge but they are not automatic, but instead are only determined after litigation in bankruptcy court. These exceptions are for cases of debt incurred as a result of fraud or willful and malicious conduct for example.

Will the Bankruptcy court send a list of the debts that have been discharged?

No, the bankruptcy court does not have the resources to send a specific list of those debts that have been discharged and those that have survived the bankruptcy, but generally the above guidelines will apply. The only type of debt that usually causes doubts as to whether or not the debt has been discharged is tax debt (generally income taxes owed to the US Treasury or State taxing authority). The IRS of State of Michigan can be contacted after the bankruptcy discharge is entered to determine just which tax liabilities were discharged via the court order and which survived the bankruptcy discharge.

Contact your Attorney.

If any questions arise as to which debts were in fact subject to the discharge order and which may have survived the bankruptcy, it is always best to contact your bankruptcy attorney for a complete analysis with the resources at your attorney’s disposal.

Detroit Bankruptcy Lawyer Walter Metzen

I have been practicing bankruptcy law in Detroit Michigan for over 28 years and have represented over 20,000 clients over my career. I am a Board Certified Specialist in Consumer Bankruptcy Law. For a free bankruptcy evaluation, call me at 313-962-4656.

I have been practicing bankruptcy law in Detroit Michigan for over 28 years and have represented over 20,000 clients over my career. I am a Board Certified Specialist in Consumer Bankruptcy Law. For a free bankruptcy evaluation, call me at 313-962-4656.