Have you been sued by Credit Acceptance Corporation?

Published • Updated

I have been practicing consumer bankruptcy in the Metro Detroit area for over 35 years. One of the most common reasons that I see for people having to file bankruptcy is when their wages are being garnished for a balance owed to Credit Acceptance Corporation for a vehicle that was repossessed or voluntarily turned in by one of my clients. It was thereafter sold at a private dealer auction and now there is a large balance due.

It’s hard enough to pay for a car that you have let alone one that you don’t have any more.

Credit Acceptance will hire a law firm to file a lawsuit against the person who entered into the contract and sue them for the difference between what was owed on the contract and what the car was sold for at the auction, after deducting repossession fees and costs, auctioneer fees and costs, storage fees, cleaning fees, additional accrued interest, etc. The amount they sue for is typically well over $10,000.

Detroit is called the Motor City for a reason. It is the automobile manufacturing company of the United States. Unfortunately, it lags behind other major cities when it comes to public transportation and metro Detroiters need reliable transportation to get to work, buy groceries, go to the doctor, etc. Many of my clients cannot afford to purchase or lease a new vehicle and they might have a less than perfect credit score and a forced to use subprime lenders to finance a vehicle purchase. This is where Credit Acceptance Corporation comes in.

Credit Acceptance does serve a purpose in that it will generally finance consumers auto purchases when other banks or financial institutions will not. But at a price. That price is very high interest rates. Generally, the rates that I see will nearly always be just shy of 25%, usually 24.99% annual percentage rate interest. This means that most of the monthly payment is going toward interest, especially in the early months of the loan which is typically amortized over 60 to as high as 84 months.

My clients tell me the cycle goes something like this. They find a decent job; one they need to help support themselves and their family. They need transportation to get to and from that job, but reliable public transportation is lacking in metro Detroit, so they need a car. They can’t afford a new car, so they look for a good used car. Good used cars are expensive as well so they need to finance their purchase so that they can keep that job. Their credit score is low, because they have been out of work and traditional lenders like Ford Credit, the large banks and credit unions refuse to finance their purchase due to that poor credit history. They resort to the subprime lenders such as Credit Acceptance, Santander, etc., because they are willing to give them a chance. The car breaks down, is totaled in an accident or is stolen in the first year of a 5- or 7-year loan. Insurance lapsed because the rates were so high, they simply could not afford the premiums. They are sued for the balance. The creditor wins by default and their wages are garnished or their bank accounts or future income tax refunds are levied against by the creditor.

I see it every day.

Fortunately, filing Bankruptcy can help. The filing of a Chapter 7 or Chapter 13 Bankruptcy petition will immediately stop the State court action against you at any point in time from being served with a summons and complaint and even after the creditor has been granted a judgment. Even if the creditor has started garnishing wages or is attempting to levy against your income tax refunds or bank accounts, the automatic stay in bankruptcy goes into effect immediately upon the filing of the case and such actions are prohibited by federal law.

Table of Contents

- How Filing Bankruptcy Stops a Garnishment From Credit Acceptance Corporation

- The Automatic Stay: The Legal “Stop Button”

- Why Auto Finance Garnishments Happen

- How Bankruptcy Stops the Garnishment Immediately

- What Happens to the Debt After Filing?

- Have you been sued by Credit Acceptance Corporation? The Bottom Line.

How Filing Bankruptcy Stops a Garnishment From Credit Acceptance Corporation

When a client walks into my office with a wage garnishment already hitting their paycheck, there is usually a sense of urgency—and understandably so. Few financial pressures feel as immediate as watching your earnings reduced before they even reach your bank account.

One of the most common garnishment situations I see involves auto finance companies, including creditors like Credit Acceptance Corporation, pursuing a deficiency balance after repossession or default. The good news is this: bankruptcy can stop that garnishment almost immediately.

The Automatic Stay: The Legal “Stop Button”

The moment a bankruptcy case is filed—whether Chapter 7 or Chapter 13—the law imposes what is called the automatic stay.

Think of the automatic stay as a court-ordered emergency brake on nearly all collection activity. That includes:

- Wage garnishments

- Bank levies

- Lawsuits

- Collection calls

- Repossession efforts

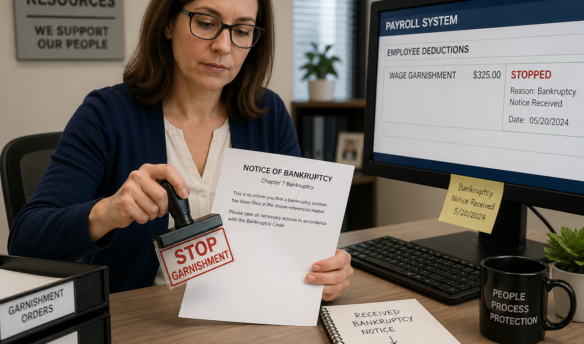

If Credit Acceptance Corporation (or any other creditor) is garnishing wages, that garnishment must legally stop once the bankruptcy is filed and notice is provided to the garnishing court and employer.

In most cases, employers will stop withholding within a pay cycle or two once they receive the bankruptcy notice.

Why Auto Finance Garnishments Happen

Auto lenders like Credit Acceptance Corporation typically pursue garnishments after one of two events:

- Vehicle repossession with a deficiency balance

After the car is repossessed and sold at auction, the remaining loan balance (plus fees) becomes a deficiency judgment. - Default judgment after a lawsuit

If the borrower does not respond to a collection lawsuit, the lender obtains a judgment, which can then be enforced through wage garnishment.

These balances can sometimes be significant, especially when vehicles are sold at auction for far less than the remaining loan amount.

How Bankruptcy Stops the Garnishment Immediately

Once your bankruptcy is filed:

- The court issues a case number the same day

- The automatic stay becomes effective immediately

- Your attorney (or you, if filing pro se) notifies the creditor and garnishing court

- The employer is directed to stop withholding wages

In practical terms, that means a garnishment from Credit Acceptance Corporation should stop very quickly after filing—often within days, depending on payroll timing.

What Happens to the Debt After Filing?

Whether the garnishment debt goes away depends on the type of bankruptcy:

Chapter 7 Bankruptcy

In many cases, deficiency balances from auto loans are discharged, meaning you are no longer legally obligated to pay them.

If the debt is discharged:

- The garnishment ends permanently

- Any remaining balance is wiped out

- The creditor cannot resume collection

Chapter 13 Bankruptcy

In a Chapter 13 repayment plan:

- The garnishment stops immediately

- The debt is folded into the repayment plan

- You repay a portion (or sometimes none) depending on income and assets

Either way, the garnishment is stopped.

Timing Matters

One important point I emphasize to clients: timing is critical.

If wages are currently being garnished, filing bankruptcy before too much is taken can preserve income that is often needed for rent, utilities, and transportation.

In some cases, we may even be able to recover money taken shortly before the filing, depending on timing and exemptions.

Have you been sued by Credit Acceptance Corporation? The Bottom Line.

If you are being sued by Credit Acceptance Corporation or any other creditor for collections, even if they have obtained a judgment against you, feel free to contact me to see if a bankruptcy filing can help you. I have filed over 25,000 personal bankruptcy cases for residents of metropolitan Detroit over the last 35 years and I offer free consultations.

A wage garnishment from a creditor like Credit Acceptance Corporation can feel overwhelming, but it is not permanent. Bankruptcy law was specifically designed to give people a reset when collections become unmanageable.

The automatic stay is powerful—it stops garnishments immediately and gives you breathing room to regain financial stability.

If you are dealing with a garnishment, the key takeaway is simple: the sooner you act, the sooner the law can protect your paycheck.